Download presentation

Presentation is loading. Please wait.

1

Caspian Strategy Institute Assoc. Prof. Dr. Fatih Macit

2

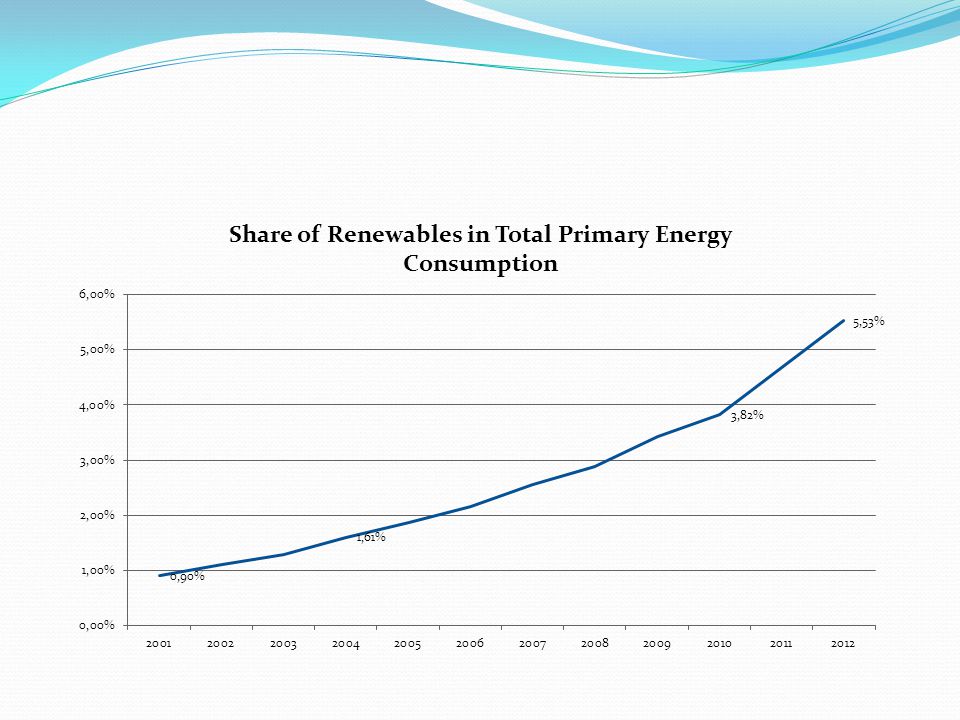

A relatively flat pattern is observed in terms of consumption of natural gas in EU-27 over the last decade. Although consumption had reached to almost 500 bcm in 2010, between 2002 and 2012 there is almost no change in total consumption. The share of natural gas in total primary energy consumption has also remained stable.

3

There are a couple of factors that contributed to this flat pattern in gas consumption. Economic slowdown that has been observed in the region since 2008. Increased use of renewables in total primary energy consumption. Improvements in energy efficiency.

6

Future economic growth, use of alternative energy sources, and improvements in energy efficiency will play an important role in terms of future gas consumption. Different institutions have different forecast for EU gas demand until 2030. The range for projections for 2020 is 190 bcm whereas the range for 2030 projections goes up to 248 bcm. Production is in a declining trend. Import demand is expected to increase.

7

VariablesElasticities Real GDP1.17 Population-0.06 Energy Intensity1.73 Share of Nuclear Energy-4.38 Share of Hydro Consumption-2.83 Share of Renewable Energy-5.19 Share of Coal-3.36

8

Low Growth Scenario: 1% growth until 2020 and 1.5% growth between 2020 and 2030. Moderate Growth Scenario: 1.5% growth until 2020 and 2% growth between 2020 and 2030. High Growth Scenario: 2% growth until 2020 and 2.5% growth between 2020 and 2030

10

The question is how will EU meet the additional import demand for natural gas. Russia is the largest supplier and will continue to be an important supplier. Only 11% of total consumption is met by LNG. LNG prices are not competitive and capacity utilization for LNG regasification plants is only 30%.

12

Caspian region will appear as an important alternative in meeting future natural gas demand of Europe and serving supply diversification. Proved natural gas reserves of the region are around 23 tcm which accounts for 12.3% of total reserves in the world. Actual production and exports are not in line with reserves. Only 4.7% of world’s total gas production comes from the Caspian region.

13

SGC is important in terms of opening a new route to EU. Although the initial amount is not big relative to the market demand, alternative sources may be added to this corridor. TANAP is an important milestone for SGC project. The line will be initially supported by Azerbaijani gas but later other sources may be added to this corridor.

14

SGC is also important for South Eastern European countries. Albania, Kosovo, and Montenegro do not have a domestic natural gas market and there is advantage for gas suppliers to construct domestic gas infrastructure.

Similar presentations