Download presentation

Presentation is loading. Please wait.

1

Oil Sands 101 ERG Victoria Jan 09 Roger Bailey

2

Alberta Tar Sands Big, Tough Expensive Job Not Economic Depends on government handouts Dirty Oil Pollutes the Environment –Air: SOx, Nox, CO 2, Climate –Water: consumption, toxic sludge –Land: Devastates Boreal forest Destroys society

3

Alberta Oil Sands World’s largest oil deposit 2,000,000,000,000 Established Reserves: 173,000,000 barrels Canada’s economic engine $70 billion invested, $70 billion planned Now 1.2 million BPD, 5 million BPD in 2030 Creates Jobs and Wealth Mining yesterday’s technology In-Situ SAGD is the future

4

What Changed? 1.Price of oil over $50 / bbl 2.“The end of cheap oil” 3.Government Policy. 4.Technology 5.Resources to Reserves

5

What Recently Changed? 1.Price of oil under $40 / bbl 2.Not “the end of cheap oil” 3.Government Policy 1.Royalties up (Syncrude + $2 billion) 2.Taxation: No accelerated CCA 3.CO2 Penalties 4.Technology: CO2 focus 5.Resources to Reserves? Economics

2.Taxation: No accelerated CCA 3.CO2 Penalties 4.Technology: CO2 focus 5.Resources to Reserves. Economics.")

6

AOSTRA Alberta Oil Sands Technology and Research Authority Alberta invested $750 million in R&D Industry matched funding and did the work Enabling Technologies –Steam Assisted Gravity Drainage (SAGD) –Cold Water Extraction (OCWE) –Consolidated Tailings (CT)

–Cold Water Extraction (OCWE) –Consolidated Tailings (CT)")

7

Alberta’s Oil Sands Areas

8

Alberta Geology

9

Alberta Oil Sands Production

10

Alberta Oil Production Source: CERI Study CAPP Backgrounder 2008

11

Alberta Oil Update Dec 2008 Source: CAPP Update Dec 2008

12

Oil Sands Projects Athabasca Mining 1,115,000 –2,977,000 Athabasca In-Situ 324,000 – 1,543,000 Cold Lake In-Situ 219,000 – 280,000 Peace River In-Situ 12,000 – 100,000

13

Mining Technology Change Truck and Shovel Hydrotransport Cold Water Extraction Consolidated Tailings

14

Athabasca – Mining Operator Project Initial Potential Albian/Shell Muskeg/Jackpine 150,000 560,000 Suncor Base Plant 280,000 550,000 Syncrude Base Plant 300,000 600,000 CNRL Horizon (2008) 135,000 577,000 Imperial Kearl (2010) 100,000 300,000 Petro-Canada Fort Hills (2011) 100,000 190,000 Total Joslyn Creek Mine(2013) 50,000 200,000

135, ,000 Imperial Kearl (2010) 100, ,000 Petro-Canada Fort Hills (2011) 100, ,000 Total Joslyn Creek Mine(2013) 50, ,000")

15

Athabasca – In Situ - SAGD Operator Project Initial Potential JACOS Hangingstone 1 0,000 30,000 Suncor Firebag 68,000 375,000 ConocoPhillips Surmont 25,000 110,000 EnCana Christina/Foster 42,000 400,000 Devon Jackfish 35,000 70,000 Husky Sunrise (2012) 50,000 200,000 OPTI/Nexen Long Lake 72,000 288,000 Petro-Canada MacKay River 22,000 70,000

50, ,000 OPTI/Nexen Long Lake 72, ,000 Petro-Canada MacKay River 22,000 70,000")

16

Cold Lake – In Situ –SAGD Operator Project Initial Potential Shell Hilda Lake (pilot) 600 20,000 CNRL Primrose 50,000 110,000 Imperial Cold Lake (CSS) 150,000 110,000 Husky Tucker 18,000 40,000 Peace River – In Situ Shell Peace River 12,000 100,000

,000 CNRL Primrose 50, ,000 Imperial Cold Lake (CSS) 150, ,000 Husky Tucker 18,000 40,000 Peace River – In Situ Shell Peace River 12, ,000")

17

Underground Test Facility (UTF) Shaft & Tunnel Access SAGD Well Pairs Horizontal Injector And Producer

Shaft & Tunnel Access SAGD Well Pairs Horizontal Injector And Producer")

18

Steam Assisted Gravity Drainage Steam injected in upper horizontal well melts the bitumen Bitumen flows by gravity down to the lower producing well Steam chamber grows as bitumen is produced Recovery over 60%

19

SAGD Applicability Resources to Reserves 352 Billion @ 6% 239 Billion @ 10% EUB Reserves in 2000 173 Billion based on SAGD Steam Assisted Gravity Drainage

20

Oil Sands Reserves

21

Steam Assisted Gravity Drainage

22

SADG needs steam. Steam Oil Ratio ~3 Steam is water and energy –Both are limited and expensive Little fresh water: saline and recycle Expensive water treatment required Energy? Gas, Co-generation? Gasification? Pitch? Nuclear?

23

SAGD CO2 Emissions Natural gas for steam ~1 GJ/barrel CO2 Emissions ~60 kg/bbl Cogeneration: –Gas turbine produces electricity –Exhaust + re-firing produces steam Cogen steam for SAGD with no CO2 CO2 in Cogen charged to electricity CO2 from Cogen less than coal

24

Nuclear Energy for Oil Sands? Nuclear for steam, electricity and hydrogen is possible but….

25

Oil Sands Projects Source: CERI Study CAPP Backgrounder 2008

26

Bitumen Upgrading Upgrading takes the black out of black oil, the tar (asphalt) Synthetic crude approximates crude oil for refineries SCO flows and distils to refinery fuel products Bitumen needs carbon out or hydrogen in Capital, energy and CO 2 intensive Refinery integration in US?

Synthetic crude approximates crude oil for refineries SCO flows and distils to refinery fuel products Bitumen needs carbon out or hydrogen in Capital, energy and CO 2 intensive Refinery integration in US")

27

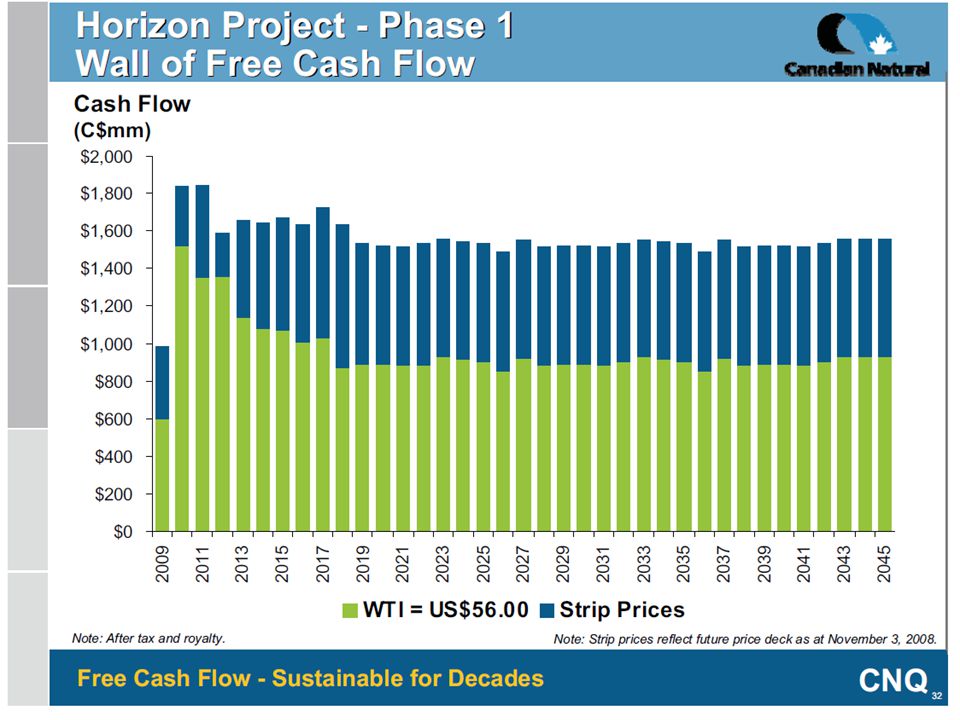

Wall of Cash Flow “Wall of Cash Flow”

28

20 Year Horizon Source: CERI Study CAPP Backgrounder 2008

32

20 Year Horizon

34

Oil Sands Challenges Environmental sustainability –CO2 costs –Natural gas limitations and costs Fiscal changes, lower returns Infrastructure limitations Workforce New Markets and Pipelines Upgrading? Moving to US refineries

35

Inflation: Capital Cost Source: CAPP Backgrounder 2008

36

Dirty Oil? Not the “End of Oil” nirvana Other oil options will be produced Oil Sands, Oil Shale, Carbonates Life Cycle Analysis: –85% of Emissions in use as fuel

37

Life Cycle Analysis

Similar presentations

–A mix of crude bitumen (semi-solid oil),>")

October 20 th, 2011.>")