Download presentation

Presentation is loading. Please wait.

1

Power Utilities in the Telecom Business in the USA: Past Failures and Future Trends Mike Oldak Vice President & General Counsel Utilities Telecom Council World Bank Sustainable Development Forum Energy Sector Day January 21, 2010 Mike.Oldak@UTC.org 202 833 6808

2

Where Are We?

3

Demand Projected To Increase 40% 21% by 2030 Sources: U.S. Department of Energy, Energy Information Administration Billon kiloWatthours Recession Impact?

4

4 Margins Projected to Fall Below Minimum Target Levels (2007) TRE (ERCOT) 2009/2016+ New England 2009/2009 RFC (MISO)* 2008/2008 AZ/NM/SNV 2009/2011 California 2009/2012 Rocky Mtn 2008/2011 SPP 2015/2016+ MRO 2009/2009 (US) New York 2011/2016+ RFC (PJM) 2012/2014 *Excludes MISO resources outside the RFC boundary Source: NERC 2007 Long Term Reliability Assessment

TRE (ERCOT) 2009/2016+ New England 2009/2009 RFC (MISO)* 2008/2008 AZ/NM/SNV 2009/2011 California 2009/2012 Rocky Mtn 2008/2011 SPP 2015/2016+ MRO 2009/2009 (US) New York 2011/2016+ RFC (PJM) 2012/2014 *Excludes MISO resources outside the RFC boundary Source: NERC 2007 Long Term Reliability Assessment")

5

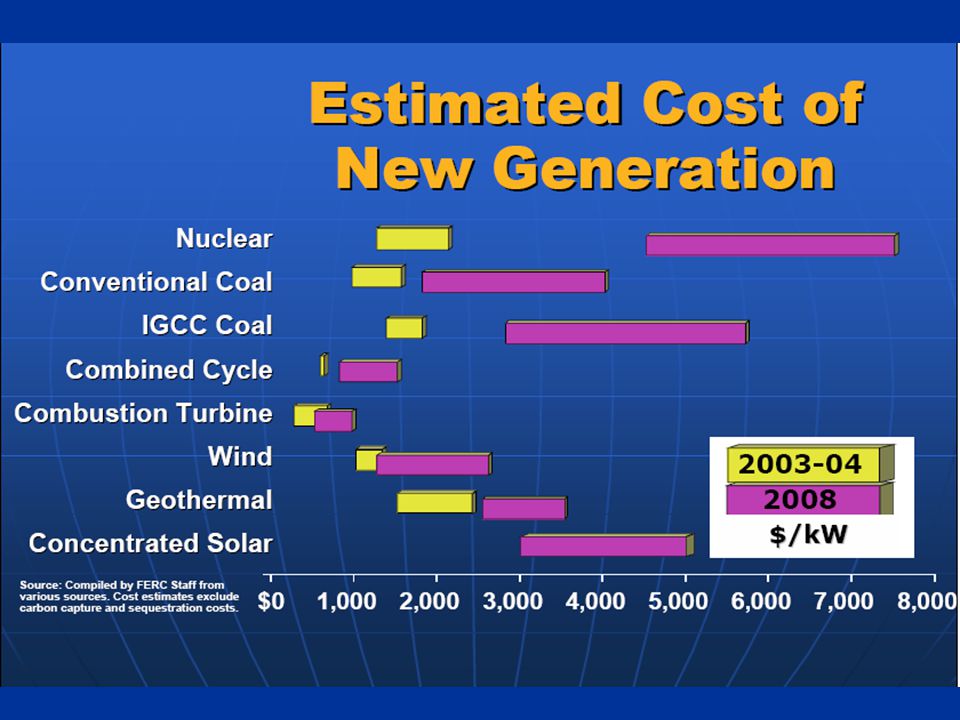

Coal Plant Cancellations / Closings 2006 - 2007 Source: NRDC: The Growing Trend Against Coal-Fired Power Plants; other publications

7

View Forward

8

President Obama’s Energy / Environmental Views Climate Change EnergyEfficiency Energy Efficiency Smart Grid Renewable Portfolio Standards 25% by 2025 Overhaul of Federal Efficiency Codes Increased Government Support 80% reduction by 2050 H.R. 2454 83% reduction by 2050 H.R. 2454 20% by 2020 In H.R. 2454 In H.R. 2454 and stimulus package

9

Utility Industry’s Future Tied to The Smart Grid Smart Grid is Smart devices and sensors from generator to end use consumer New awareness and control over all aspects of the grid Advanced communication linking all parts of the grid

10

Utility Telecom Provides Unique Benefits Multiple Revenue Streams Aggregate demand response to reduce wholesale market prices Provide consumers with information and tools to optimize usage Relieve congestion at transmission and distribution level Avoid or defer G, T & D infrastructure investments Optimize use of existing resources Coordinate integration of new renewables and storage devices Improve customer, distribution and grid reliability Use smart grid fiber / spectrum to support other broadband needs Utilities are uniquely positioned to optimize the new smart grid and maximize the benefits from smart grid investments

11

Value For Consumers and Utilities Baltimore Gas & Electric

12

How Smart Grid and Smart Rates Can Help Critical Peaks

13

Dynamic Peak Pricing: Weekdays (excluding Holidays) 2 Baltimore Gas & Electric 2009 Pilot Pricing All – in Rate* Critical $1.30425 Peak $0.14425 Off-Peak $0.09425 * Includes generation, transmission and delivery $1.30 $0.14 $0.09

2 Baltimore Gas & Electric 2009 Pilot Pricing All – in Rate* Critical $ Peak $ Off-Peak $ * Includes generation, transmission and delivery $1.30 $0.14 $0.09")

14

Peak Time Rebate: Weekdays (excluding Holidays) Schedule R summer rates are $0.14 / kWh for all summer hours Up to 12 critical peak days will be called by 6 p.m. the prior day Customers who use less during the critical period (2 – 7 p.m.) on any critical peak day will receive a rebate. Two levels being tested: $1.75/kWh and $1.16/kWh 3 Baltimore Gas & Electric 2009

on any critical peak day will receive a rebate. Two levels being tested: $1.75/kWh and $1.16/kWh 3 Baltimore Gas & Electric")

15

Hours in Each Summer Pricing Period 60 hours of higher “Critical Peak”

16

Ba 16 Actual Load Shapes for Participants and Control Group during Critical Peak Event

17

Summer 2008 Pilot Smart Energy Pricing - Peak Demand Reductions * 17 Orb & Switch Orb Only No Tech Orb & Switch No Tech Orb & Switch Orb & Switch Orb & Switch No Tech No Tech Orb Only Orb Only % Change in Critical Peak Demand Low Rebate $1.16 /kWh High Rebate $1.75 / kWh DPP Rate

18

Estimated BG&E Deployment Costs $ 482 Million (2009-14) 18 $10 other $329 Meters and Modules $99 Information Technology $14 Communications $30 Smart Energy Pricing

18 $10 other $329 Meters and Modules $99 Information Technology $14 Communications $30 Smart Energy Pricing")

19

Customer Savings Greatest Benefit Projected Life-cycle Saving >$2.6 B 19 $661 $580 $452 $408 $204 $117 $104 $61 $49 Avoided Generation Capacity Cost Capacity Price Mitigation Energy Conservation Operational Savings Avoided Capital Expenditures Avoided Transmission Infrastructure Energy Price Mitigation Energy Revenues Avoided Distribution Capacity Cost ($'s in millions)

")

20

BG&E Residential Bill Impact 20 Over the life of the recovery period, the average monthly electric and gas surcharge is projected to be $1.24 and $1.52, respectively $0.00

21

Lesson from the Past Utilities and Telecom In the 1990s utilities tried to compete with commercial telecom carriers – results were generally poor Strengths of utilities Efficient construction of backbone energy and telecom system Ability to ensure highest reliability Able to finance huge projects at low-risk rates Operate in a regulatory environment where decisions will be subject to review for both correctness and cost containment Strength of commercial telecom carriers Willing to take risks and act quickly No need to seek regulatory review Part of core business Solid understanding of business models

22

Role for Utilities Leverage core capabilities Build out system as a carrier’s carrier Leverage existing assets Dark fiber Existing infrastructure Some utility technologies lend themselves, others do not! Leverage economies of scope and scale Uniquely positioned to access multiple revenue streams from investments Relationships with local governments, authorities Ability to energize a large, geographically diverse workforce

Similar presentations

Mayor Alex Knopp November 18, 2004.>")

395-4143.>")