Download presentation

Presentation is loading. Please wait.

1

Property Tax Levy Cap Chapter 97 of the Laws of 2011

2

The tax levy cap- begins in 2012-13 School Fiscal Year In effect through at least 2016-17. Thereafter, it remains in effect only so long as regulation and control of residential rents and evictions (i.e., rent control) laws are in place. Chapter 97 leaves the current contingency budget requirements/restrictions in place

laws are in place. Chapter 97 leaves the current contingency budget requirements/restrictions in place.")

3

Tax Levy Limit Prior year tax levy (x tax base growth factor, if any) + Payments in lieu of taxes receivable during prior year – Taxes levied for exemptions during prior year (not ERS & TRS) = Adjusted Prior Year Tax Levy x Allowable levy growth factor (lesser of 2% or CPI) – Payments in lieu of taxes receivable in the coming year + Available carryover, if any = “Tax Levy Limit”

+ Payments in lieu of taxes receivable during prior year – Taxes levied for exemptions during prior year (not ERS & TRS) = Adjusted Prior Year Tax Levy x Allowable levy growth factor (lesser of 2% or CPI) – Payments in lieu of taxes receivable in the coming year + Available carryover, if any = Tax Levy Limit")

4

+ Dollar amounts attributable to coming year exemptions = Allowable tax levy prescribed by Chapter 97 of the Laws of 2011 (with a simple majority vote)

")

5

Allowable Levy Growth Factor = Lesser of: 1.02 OR (1 + Inflation Factor); Minimum of 1.0. Inflation Factor = CPI change, carried out four decimal places. Source: US Department of Labor Available Carryover = (Prior year tax levy limit – prior year tax levy), but no greater than (.015 x prior year tax levy limit). Districts may use taxing authority from the prior school year to increase the subsequent year’s tax levy if taxes were increased in the prior school year by less than the amount allowed by the cap. Maximum carryover increase is the lesser of actual available carryover or 1.5% Source: NYS Office of the Comptroller Quantity Change Factor = The percentage by which the full value of the taxable real property in the school district increases due to physical or quantity change, compared with the prior year tax roll (growth in full value due to new construction, additions and improvements to real property, etc.). Source: New York State Tax and Finance Department Tax Base Growth Factor = 1 + Quantity Change Factor; only calculated if quantity change factor is a positive number. Determined by Office of Real Property Tax Services Definitions

, but no greater than (.015 x prior year tax levy limit). Districts may use taxing authority from the prior school year to increase the subsequent year’s tax levy if taxes were increased in the prior school year by less than the amount allowed by the cap. Maximum carryover increase is the lesser of actual available carryover or 1.5% Source: NYS Office of the Comptroller Quantity Change Factor = The percentage by which the full value of the taxable real property in the school district increases due to physical or quantity change, compared with the prior year tax roll (growth in full value due to new construction, additions and improvements to real property, etc.). Source: New York State Tax and Finance Department Tax Base Growth Factor = 1 + Quantity Change Factor; only calculated if quantity change factor is a positive number. Determined by Office of Real Property Tax Services Definitions.")

6

Exemptions Capital Tax Levy = Tax levy necessary to support capital local expenditures Capital Local Expenditures = The tax levy associated with budgeted expenditures resulting from the construction, acquisition, reconstruction, rehabilitation or improvement of school district capital facilities or capital equipment, including debt service and lease expenditures, and transportation capital debt service. Court Orders = Tax levy necessary for expenditures resulting from court orders or judgments arising out of tort actions for any amount that exceeds 5% of total tax levied in prior school year

7

Exemptions ERS Costs = Tax levy necessary for expenditures for coming school year for employer contributions caused by growth in the system average actuarial contribution rate, minus two percentage points. TRS Costs = Tax levy necessary for expenditures for coming school year for employer contributions caused by growth in the normal contribution rate, minus two percentage points The pension cost exclusion applies only when ERS and TRS employer contribution rates increase by more than 2 percentage points over the prior year. For example, if an employer contribution rate for ERS or TRS increased by 2.2 percentage points, only an amount equal to applicable salary expenditures times.002 would be excluded from the tax levy cap. If an employer contribution rate increased by 1.98 percentage points over the prior year, no exclusion would be allowed from the cap on the tax levy for pension cost increases.

8

One area in which schools have almost no discretion over spending is the mandatory contributions they make to the state pension systems. Teacher Retirement System (TRS) contribution rates increased from.36% of payroll in 2002-03 to 11.84% in 2012-13.

contribution rates increased from.36% of payroll in to 11.84% in")

9

Employees Retirement System (ERS) ERS rates increased from 1.3% of payroll in 2002-03 to 18.9% of payroll in 2012-13.

ERS rates increased from 1.3% of payroll in to 18.9% of payroll in")

10

Pension Calculation: ERS 18.9% - 16.3% = 2.6 ( SFY 12-13) (SFY 11-12) Percentage Points Difference 2.6 - 2.0 = 0.6% % point diff. Local responsibility Excludable Portion

11

ERS Exclusions:

12

TRS Exclusions

13

TRS Exclusion It has been determined that there will be no TRS Exclusion for School Districts. The TRS rate did not increase over 2% from 2011-12 to 2012-13 Rate 11-1211.11% Rate 12-1311.84%

14

Pension Exclusion Calculator Brocton Central

15

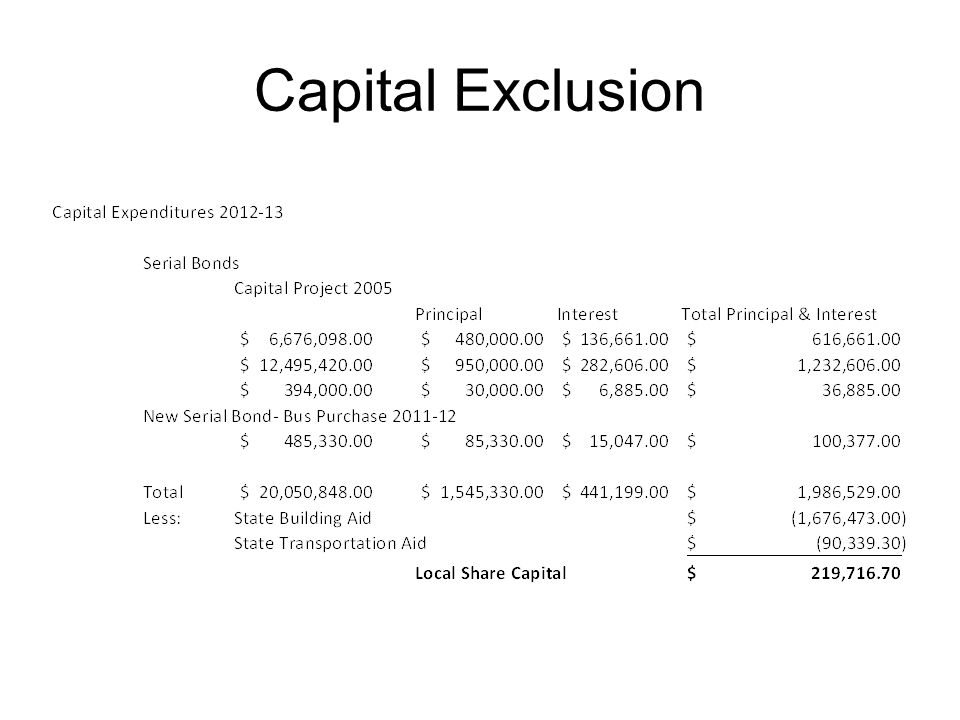

Capital Exclusion

18

Summary Brocton’s Tax Levy Limit before exclusions=$4,199,886 Plus Exclusions= 226,145 Total Allowable Tax Levy 2012-13$4,426,031 Dollar Increase from prior yr. levy……………..$112,711 Percentage increase from prior yr. levy…………… 2.61% Available carry-over (limited to 1.5% of levy limit)….. $62,998.29 Lesser of actual available c/o or 1.5%

….. $62, Lesser of actual available c/o or 1.5%.")

19

Override –School Districts School districts must put the override to their budget voters Requires budget to pass by 60% Budget that does not exceed cap must pass with simple majority (>50%) If no budget approved, contingency budget may not include a levy higher than prior year’s levy

If no budget approved, contingency budget may not include a levy higher than prior year’s levy")

20

Questions?

Similar presentations