Download presentation

Presentation is loading. Please wait.

1

Sources of Government Revenue

2

The Economics of Taxation : Economic Impact of Taxes

Taxes/Other government revenues affect: resource allocation, consumer behavior, nation’s productivity Growth

3

Economic Impact of Taxes : Resource Allocation

Affects factors of production A TAX placed on a good at the factory = rise in production cost Supply curve shifts to the left If demand stays the same = equilibrium price goes op

4

Economic Impact of Taxes: Behavior adjustment

TAXES affect the economy Encourage or discourage certain activities SIN Tax: high percentage tax that raises revenue while reducing consumption of a socially undesirable product

5

Economic Impact of Taxes: Productivity and Growth

Taxes affect productivity and economic growth: Change incentives to save, invest, and work Why people favor lower taxes….

6

Economic Impact of Taxes: The Incidence of a Tax

“Final Burden of the Tax” I.e. Utility company: Raise rates: consumer bears the burden (easy if demand is inelastic) Rates are regulated = Shareholders receive smaller dividends; postpone raises (more elastic = producer will absorb the tax)

Rates are regulated = Shareholders receive smaller dividends; postpone raises. (more elastic = producer will absorb the tax)")

8

Criteria for Effective Taxes

TAXES are effective when they are: Equitable Simple Efficient

9

Criteria for Effective Taxes

Criterion 1: Equity or fairness Taxes should be IMPARTIAL and JUST Fairness is subjective Taxes are considered FAIRER Fewer loopholes: exceptions, deductions, and exemptions

10

Criteria for Effective Taxes

Criterion 2: Simplicity Tax LAWS should be EASY to understand Individual income taxes: the taxes on peoples earnings Complex tax = dislike Sales tax: general tax levied on most consumer purchases; paid at the time of purchase Anyone purchases = pay tax

11

Criteria for Effective Taxes

Criterion 3: Efficiency Easy to administer and successful at generating revenue Individual income tax Less efficient: toll booths Luxury taxes

12

Two Principles of Taxation

Benefit Principle: those who benefit from government and services should pay in proportion to the amount of benefits received Gas tax (built in) pay more if you drive more Two limitations: Many gov’t services provide the greatest benefits to those who can least afford to pay for them Benefits are hard to measure

pay more if you drive more. Two limitations: Many gov’t services provide the greatest benefits to those who can least afford to pay for them. Benefits are hard to measure.")

13

Two Principles of Taxation

Ability-to-Pay Principle: people should be taxed according to their ability to pay, regardless of the benefits they receive. Two factors Recognizes that societies cannot always measure benefits Assumes that people with higher incomes suffer less discomfort paying taxes than people with lower income

14

Types of Taxes Proportional: imposes same percentage rate of taxation on everyone Progressive: imposes a higher percentage rate of taxation on people with high incomes than on those with low incomes Regressive: imposes a higher percentage rate of taxation on low incomes than on high incomes

15

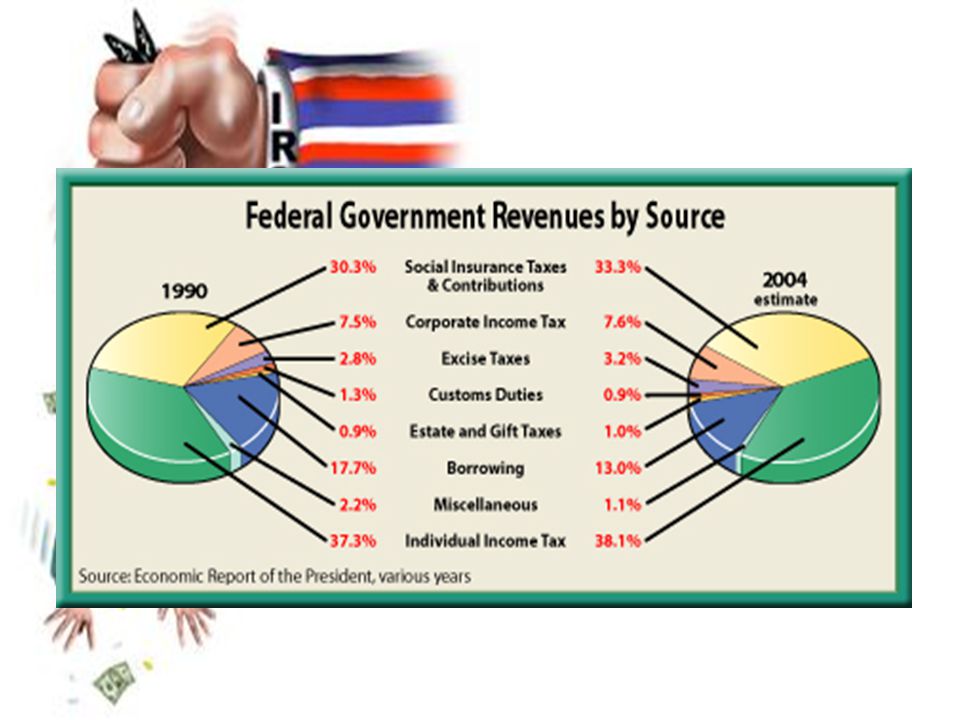

Figure 9.3

16

The Federal Tax System

17

IRS (Internal Revenue Service)

part of the Treasury Department

18

Individual Income Taxes

Fed. Gov’t collects 45% of its revenue from Individual income taxes Paid over time through payroll withholding system Before April 15th each year, an employee must file a tax return: an annual report to the IRS summarizing total income, deductions, & taxes withheld by employers

19

Individual Income Taxes

Progressive tax Individuals earning higher incomes pay higher tax rates Progressive Tax that ranges from 15% -39.6%

20

FICA: What is FICA? And why does it take part of my paycheck

FICA stands for Federal Insurance Contributions Act FICA tax includes Social Security (6.2% of wages) & Medicare (1.45% of wages) 2nd largest source of Gov’t revenue

& Medicare (1.45% of wages) 2nd largest source of Gov’t revenue.")

21

FICA Social Security is a proportional tax up to $65,400 (the capping point) and then it is regressive Medicare is not capped; it’s proportional at all levels of income Total FICA tax = 7.65%

22

Corporate Income Taxes

3rd largest category of federal taxes Corporation is recognized as a separate entity Rates vary from 15% -35% (slightly progressive)

")

23

Other Federal Taxes Excise Tax: tax on the manufacture or sale of certain items, such as gasoline and liquor Estate Tax: tax the gov’t levies on the transfer of property when a person dies Gift Tax: tax on gift of money/wealth paid by person making gift

24

State and Local Tax Systems

25

State Government Revenue Sources

Intergovernmental Revenues - money from federal gov’t Sales tax - general tax on consumer purchases Employee Retirement Contributions Individual Income Taxes (not all states)

")

27

STATE SALES TAX States with the Highest Sales Tax: Mississippi

Rhode Island Washington Texas Illinois

28

STATE SALES TAX States Without a State Sales Tax: Alaska Delaware

Montana New Hampshire Oregon

29

Advantages of Sales Tax

Effective way to raise large sums of money Difficult to avoid because it affects large numbers of consumers Relatively easy to administer - merchant collects at point of sale

30

Local Property Taxes Second largest source of revenue for local governments Real Property: includes real estate, buildings, & anything permanently attached

31

Local Property Taxes Tangible Personal Property: includes tangible items, not permanently attached. Intangible Personal Property: property with invisible value, such as stock, bond, patent, check

32

Examining Your Paycheck

Payroll withholding statement: the summary statement attached to a paycheck that summaries income, tax withholdings, and other deductions

34

State & local governments rely heavily on sales tax for revenues

QUESTION: WHY ARE STATE & LOCAL GOVERNMENTS LOSING MONEY TO THE INTERNET??? State & local governments rely heavily on sales tax for revenues State & local governments already lose $3.3 billion each year to untaxed interstate sales This figure will increase as more sales are made over the Internet Should there be an Internet sales tax??? How would it work?

Similar presentations